As a Canadian citizen who’s recently moved to Texas, this topic is near and dear to my heart.

For my Canadian and other international friends/investors, I wanted to provide an in-depth article covering why international investors love the US, what are some considerations and what steps they can take to start investing.

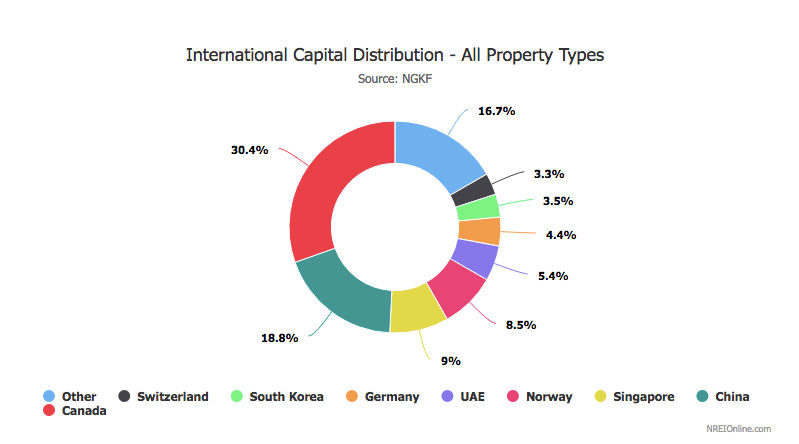

Source: National Real Estate Investor

Real estate investors from all over the world actively (and passively) invest in the robust US market. I’ve covered some reasons below:

- USA, USA, USA!

- Stable and Regulated Markets

- Market Size

- Diversity of Opportunities

- Global Diversification

- Top Performing Asset Class

- Family Reasons

- USA, USA, USA!: Global investors love investing in the US and, often times, pay a premium as they hold US real estate in high regard. From a personal perspective, I have observed that my international friends (Canadian and otherwise), often have deeper knowledge of the US economy than their own countries! This goes to show you the importance and prestige associated with investing in the US.

- Stable and Regulated Markets: The US market is seen as a safe haven and gold standard for global real estate investing. Unlike the commodity driven economies (Middle East, South America) or Europe (Brexit), the US economy is viewed as a well-oiled machine providing long-term asset growth. The rule of law in the US is of utmost importance as many investors come from countries where the enforcement of law is not upheld.

- Market Size: Not only is the US the biggest economy in the world, but individual states like Texas and California are vibrant, strong and huge markets. To give you an idea of perspective, California is ranked #6 and Texas is ranked #10 in the list of global economies.

- Diversity of Opportunities: The sheer size of the market ensures a diversity of opportunities that are not offered anywhere else in the world. Every niche is well represented and the associated market depth ensures that assets at all stages of the lifecycle are well represented and easily investable.

- Global Diversification: The US economy welcomes foreign capital and has a business friendly regulation structure. Unlike many countries, investors face minimal capital movement restrictions. This allows foreign investors to diversify their portfolios and currency exposure while sheltering assets in a safe, stable and secure economy.

- Top Performing Asset Class: Investors understand real estate, they see it, feel and know that multifamily investing is one of the proven ways of building long-term wealth. We purchase assets that are already generating cash returns. Our strategy is to make improvements and introduce efficiencies on top to make a good asset a great one. Our investors understand that this is not just an investment idea but an asset class that has proven its worth over time, across cultures and throughout the various stages of the business cycle.

- Family Reasons: Many investors, including those I know personally, have spouses/partners and children in the US or frequently travel to the US. As such, they want positive cash flow assets that will grow their long-term portfolios. This is especially true for investors from countries where capital movement is restricted especially regarding how much money can be transferred to the US.

What are some of the considerations that investors from abroad must think about in deciding to invest here?

- Capital Restrictions

- Currency Risk

- Political and Regulatory Environment

- Legal and Tax

Capital Restrictions: As mentioned earlier, many countries have capital controls that restrict how much investors can move from their home country to the US. This affects the pace at which these investors can grow their US-based portfolios.

Currency Risk: Most global investors seek to diversify across geographies and currencies to negate currency risk. Nonetheless, currency risk is an issue that investors need to be aware of when investing in the US market.

Political and Regulatory Environment: With a highly regulated and transparent market, the US is a stellar economic performer and real estate, as an asset class, has performed remarkably well in the US.

Legal and Tax: These issues are important for an investor to understand as laws and taxation policy can differ from country to country. In particular, investors need to ensure that they can understand or get the right help to understand legal communications and contracts. Essentially, as in all legal cases, investors need to ensure that they understand what they are agreeing to before signing any documents.

How can Canadian investors participate in a US-based real estate private equity investment?

This is not intended to be a formal opinion of tax consequences because as we all know the CRA loves to keep changing its policies to keep Canucks on their toes.

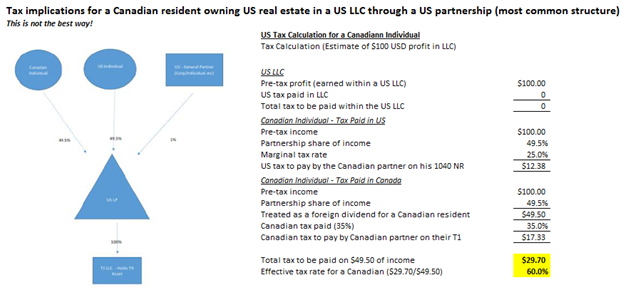

On May 26, 2016 the CRA announced that the US LLP/US LLLP would now be classified as a corporation for Canadian tax purposes, similar to US LLCs. This will results in instances of, potential, double taxation (covered below) for Canadian investors.

Facts and Assumptions

- Boardwalk Wealth generates investment capital from US and Canadian citizens;

- US marginal tax rate: 25%;

- Canadian marginal tax rate: 35%;

- Only personal and corporate tax implications will be discussed i.e. no commentary on estate tax and state/local taxes;

The ideal structure for Canadian investors is the US LP structure. This provides the asset protection for limited partners and creates a cost-effective strategy for Canadian partners because the CRA recognizes the LLC as a foreign corporation i.e. double taxation if a Canadian investor invests through an US LLC.

The overview below was provided by our trusted cross-border CPA and provides a great overview for Canadians.

The above is the most common structure used by Canadians. It is not the best way as it results in a massive amount of tax drag (i.e. super-high taxes).

CRA considers both single and multi-member US LLCs to be corporations for Canadian tax purposes. The IRS treats a US LLC as a flow through entity unless the tax payer elects to be treated as a US Corporation.

As a result of this difference, Canadians owning US LLCs will be double-taxed on the same income earned with the LLC. This is because the CRA recognizes the US LLC as a foreign corporation. Hence, the LLC distributions would be considered would be treated as a foreign income which is not subject to a Canadian dividend tax credit or a foreign tax credit.

As a result, double taxation arises for the Canadian tax payer. In addition, regardless of whether a US LP, US LLP or a US LLLP is used as another level in the organization chain, the CRA deems the Canadian tax payer as owning an indirect share of a US LLC.

As illustrated in the above structure, due to double taxation the effective tax rate ends up being 60% for a Canadian tax payer. In addition the LLC is not entitled to the benefits of the Canada-US Tax Treaty (“Treaty”), as the Treaty is applied at the member level.

For the reasons mentioned above, US LLCs may not be the most advantageous vehicles for Canadian residents doing business in the US.

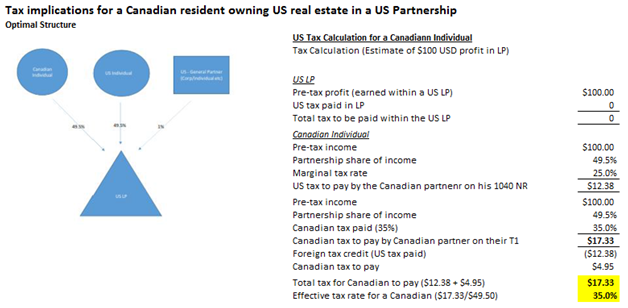

This structure is optimal.

The investment is held in a US LP. The IRS recognized a US LP as a flow-through entity for US tax purposes. As such, any income earned within the US LP is not taxed within the LP and flows up the organization chain to the partner.

Since the IRS recognizes the US LP as a flow-through entity, any profit would not be taxed at the partnership level, unless elected otherwise.

The US LP is one of the few entity structures that is considered a flow-through for both US and Canadian tax purposes.

The asset held within the US LP will provide protection for limited partners and will allow for US rental income to flow-through to the Canadian and US tax partners.

As illustrated above, since the CRA recognizes the US LP as a flow-through entity, it does not create a double taxation situation. This is because this structure allows for the use of foreign tax credits.

Since all the income and gains are being recognized at the partner level, any taxes paid on the Canadian taxpayer’s US personal tax return will be deductible on their Canadian personal tax return.

The use of FTC (foreign tax credit) would results in a significantly lower effective tax rate – 35% vs. 60% in typical LLC structure – for Canadian investors.

Care must be noted that a Canadian investor will still need to go through all the steps in the next section (barring the US LLC parts as those are covered above).

How can foreign investors participate in a US-based real estate private equity investment?

Our preferred CPAs have extensive experience in helping international investors invest and run businesses in the US. We can also advise your existing CPA if the need arises. Below, I have outlined a general guide for participating in US-based real estate private equity investing for international investors.

- Incorporate US-based LLC / Corporation

- Apply for EIN (Employer Identification Number), Register the LLC with Various Required Agencies

- Execute an Operating Agreement Among Partners

- Apply for ITIN (Individual Taxpayer Identification Number) or Social Security Number

- Open US-based Bank Accounts

- Filing the LLC US Tax Returns (Federal, State and City) and Personal Tax Returns for all Partners

- Tax Treaty Benefits Are Available

For foreign investors, only two structures are available: LLC or corporation. The former – LLC – is preferred as it avoids double taxation and offers the most tax efficiency.

Without going into the minutiae of tax laws, a single owner LLC is considered a disregarded entity and treated as a personal business for tax purposes. Hence, it loses most of the LLC benefits, and therefore it is best to have a minimum of 2 partners. With a minimum of 2 partners, all the tax benefits can now come into play.

The equity split does not matter. For instance, an LLC could have 50/50, 1/99, 40/60 or any other split. In our experience, most foreign investors tend to open these LLCs with their spouses or partners.

If that makes your head spin, don’t worry. We’ve got specialists who can easily cover this for you at very affordable rates. Plus, these are one-time costs.

Once the LLC is incorporated, the investor has to apply for an EIN (Employer Identification Number) and draft an operating agreement. Although this sounds daunting, our preferred CPAs and lawyers have extensive experience in this area and can help you set this up in under a day.

It is not uncommon to find overseas investors who already have a social security number, if they have lived in the US for work. However, if they don’t have one, they will need to apply for an ITIN. Each individual partner in an LLC needs to apply for an ITIN. This can take up to 60 days. Our experience indicates that most clients are able to get their ITIN within 4-6 weeks.

Once the EIN, operating agreement and ITIN are available, a foreign investor can open a US-based bank account. Due to our extensive banking relationships, we can help you in opening the right bank accounts with global banks that have exceptional customer service and online access.

The LLC needs to file returns as well as partners have to file personal tax returns. The K-1 (tax return for syndicate partner) often has significant deductions that results in paper losses each year, while you keep making cash flow, before a sale occurs, say in 5 years. Hence, those losses can be offset against future gains to reduce the tax bill.

Investors need to consult with their local professionals to determine tax and related disclosure requirements. For US legal structures – asset protection strategies – US-based legal professionals can provide the best advice.

In summary, commercial real estate has proven its resilience and has continuously been one of the top-performing asset classes. Investors should understand their constraints before investing and seek professional advice. Our preferred advisors have extensive experience and can help make the entire process smooth and efficient.

References:

- Investing In US From Abroad (Thompson Investing)

- How to Invest in U.S. Real Estate as a Foreigner (REtipster)

- California Passes France As World’s 6th-Largest Economy (Fortune)

- Texas (Forbes)

- Where Are Foreigners Buying Real Estate in the United States (Credit Sesame)

- Canadians beware! United States limited liability companies may be hazardous to your tax health (Moodys Gartner)