PPM Outside Structure: The Regulatory Side Of A Deal

In this first part of our series, you’ll learn about how the PPM outlines the regulatory side (or outside structure) of an investment vehicle.

When reading through a PPM, you see the following sections:

- Summary of the Offering

- How to Review the Offering

- Investor Suitability Standards

- Regulations and Investor Qualifications

- Summary of the Company

To properly understand the deal, you need to go through them all.

We’ll talk about the significance of each, one at a time, with examples.

* Note: every PPM is unique, so you may not see EXACTLY the same thing as our examples, but we’re highlighting big-picture items that are going to be covered one way or another on basically every PPM you’ll read.

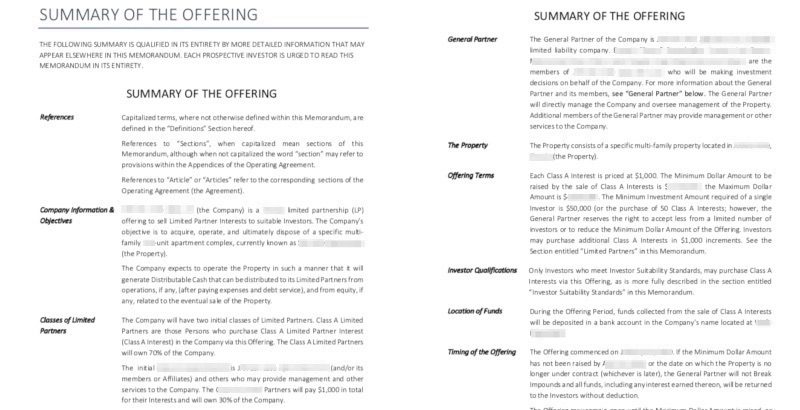

Summary of the Offering (Ground Zero)

Sometimes shortened to “Summary Offering”, this is your introduction to how the syndication company is being structured to manage the investment.

A typical summary offering includes:

Company Information and Objectives

The name of the company and clear objectives of how the company is planning to exit the property.

Classes of Limited Partnership and Equity Split

As the passive investor this is key to knowing where you fall into the structure of the deal. What are the different classes within the partnership and what to expect for payment? How the deal is split? Is it 70/30, 60/40, etc. This will depend from deal to deal and that is why it’s important to have a clear understanding, so you’re not surprised when the property is liquidated.

Use of Proceeds

This is imperative. As an investor, you’ll want to know exactly how the company or LLC plans to purchase the property, improve, operate, and ultimately dispose of the property.

Risk Factors and Conflict of Interest

This is so you know where General Partners and Limited Partners stand, as well as the risks associated with the property.

The Class A Limited Partners may have conflicts of interest with the Class B Limited Partner and the General Partner; who have interests in earning their own distributions and fees.

Liquidity

Here is where you will have a clear understanding of how liquid the property really is (which is typically ‘zero’).

A multifamily syndication is a great investment, but a drawback is its lack of liquidity. You should be prepared to stay in the property for the entire holding period. As there is typically no market to sell your holding to.

1031 Exchange

What is a 1031 exchange?

Broadly stated, a 1031 exchange (also called a like-kind exchange or a Starker) is a swap of one investment property for another.

Investors will not be able to 1031 exchange into the property. However, at the time of sale, the General Partner may call for a vote of the Limited Partners to approve exchange of the Property for another investment property under 1031 exchange rules

This would require a majority vote and you as the LP would generally be able to exit upon a 1031 exchange if you didn’t wish to proceed.

How to Review the Offering

There is where you will be able to understand the offer and ensure that you fit into the business model.

Look at the following:

Limited Partner Agreement

This describes how the Company will be run, and supersedes all previous agreements that may have been adopted by the Company.

Subscription Agreement

This contains the investor’s representations and warranties to their qualifications and suitability to invest in this Offering, the amount the investor is planning to invest, and the General Partner’s acceptance of the investor as a Limited Partner of the Company.

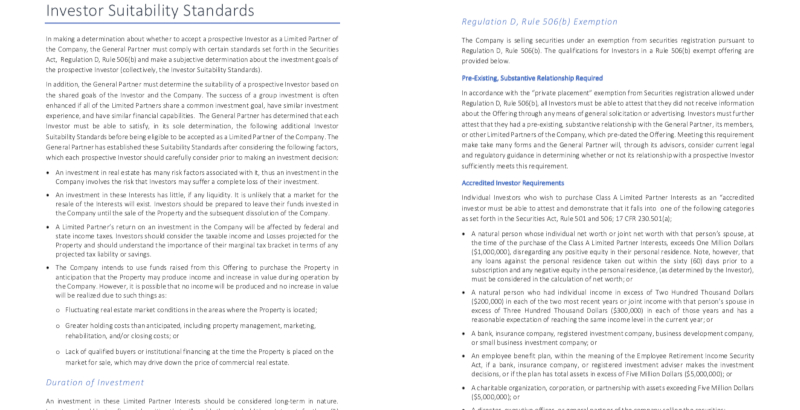

Investor Suitability Standards

In making a determination about whether to accept a prospective investor as a Limited Partner of the Company, the General Partner must comply with certain standards set forth in the Securities Act. Part of this is determining if the investment is suitable for the investor or not.

Type of SEC Offering: 506B vs 506C

Real Estate syndications have to be registered with The U.S Securities and Exchange Commission and fall under Rule 506 of Regulation D.

Under Rule 506(b), a “safe harbor” under Section 4(a)(2) of the Securities Act, a company can be assured it is within the Section 4(a)(2) exemption by satisfying certain requirements, including the following:

- The company cannot use general solicitation or advertising to market the securities.

- The company is allowed to sell to an “unlimited” amount of accredited investors and up to 35 non-accredited but sophisticated investors. A sophisticated investor is an investor who has a sufficient amount of capital and experience in these types of investments, but is not accredited.

Under Rule 506(c), a company can broadly solicit and generally advertise the offering and still be deemed to be in compliance with the exemption’s requirements if:

- The investors in the offering are all accredited investors.

- The company takes reasonable steps to verify that the investors are accredited investors, which could include reviewing documentation, such as W2s, tax returns, bank and brokerage statements, credit reports, etc

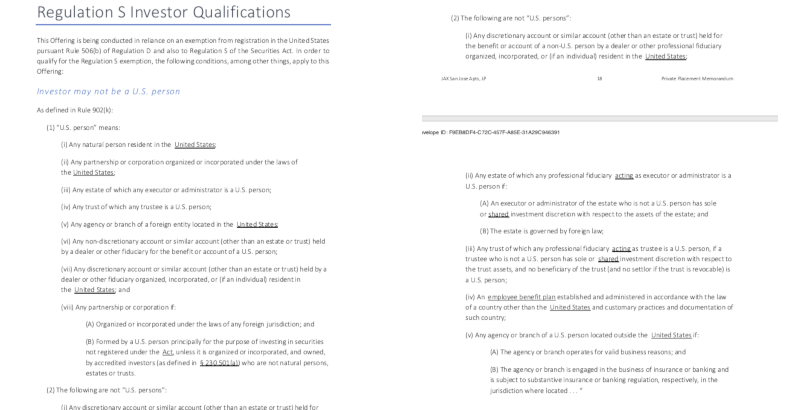

Regulations and Investor Qualifications

SDIRA Account Holders

For an entity such as an Individual Retirement Account (IRA) or Self Employed Person (SEP) Retirement Account, all of the beneficial owners must meet one of the above standards. The beneficial owners may be either natural persons or other entities if each of them meet one of the definitions above.

Unsuitable for 1031 Exchange

As mentioned before, a 1031 exchange is a tax deferment strategy for capital gains which is used by real estate investors.

If you were to exercise this investment strategy upon sale of a property or entity, one would have to declare a new property (typically within 45 days) one plans to invest in. Upon the sale of the original property those capital gains would be deferred to the next property.

However, it should be noted that this is an unlikely scenario and any investor who is looking to roll capital gains over into a new property probably shouldn’t invest in the syndication in the first place.

Any syndicator who promises to do a 1031 exchange in all likelihood lacks experience and should be vetted further before you proceed.

Is foreign investment allowed?

Disqualifying events are broadly defined to include such things as criminal convictions, citations, cease and desist or other final orders issued by a court, state or federal regulatory agency related to financial matters, Investors, securities violations, fraud, or misrepresentation.

It is up to the General Partners to know and check out all investors in the deal and make sure that they are in compliance with ALL regulations.

This is known as KYOC (know your own customer). The General Partners will validate investors’ information as they see fit.

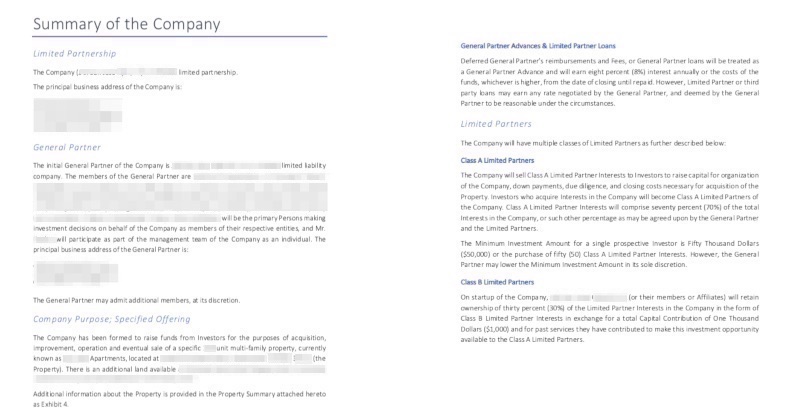

Summary of the Company

The most important section here is the Company Purpose and Specified Offering.

Financing

The General Partner anticipates the use of institutional financing to acquire the Property and to finance capital improvements. The proposed lender’s term sheet may be available on request, however, the actual loan terms will not be known until the rate is locked and/or the Property is acquired.

The General Partner reserves the right to accept different commercially available loan terms or to change lenders as necessary to acquire and subsequently refinance or supplement the loan on the Property.

Funds raised from offerings will be used to finance the down payment, closing costs, due diligence expenses, General Partner’s acquisition fees, improvements and operating reserves related for the Property and to reimburse the General Partner or its members for any expenses they may have advanced related to acquisition of the Property. In addition, the members of the General Partner may act as guarantors on the acquisition loan for the Property.

This will vary from sponsor to sponsor and you’ll just want to familiarize yourself with the specifics of the deal.

GP Advances and LP Loans

Deferred General Partner reimbursements and fees, or General Partner loans, will be treated as a General Partner Advance and will earn a percentage of interest annually or the costs of the funds, whichever is higher, from the date of closing until repaid. However, Limited Partner or third party loans may earn any rate negotiated by the General Partner, and deemed by the General Partner to be reasonable under the circumstances.

Limited Partners

It is typical in the syndication model for the Company to sell Class A Limited Partner Interests to investors to raise capital for organization of the Company, down payments, due diligence, and closing costs necessary for acquisition of the Property.

Every deal is structured differently. Here is a hypothetical example of a deal:

Class ABC Limited Partner – Interests will comprise seventy percent (70%) of the total Interests in the Company, or such other percentage as may be agreed upon by the General Partner and the Limited Partners. The Minimum Investment Amount for a single prospective Investor is $50,000 or the purchase of fifty Class A Limited Partner Interests. However, the General Partner may lower the Minimum Investment Amount in its sole discretion.

Class XYZ Limited Partner – On startup of the Company, COMPANY LLC (or their members or Affiliates) will retain ownership of thirty percent (30%) of the Limited Partner Interests in the Company in the form of Class B Limited Partner Interests in exchange for a total Capital Contribution of One Thousand Dollars ($1,000) and for past services they have contributed to make this investment opportunity available to the Class A Limited Partners.

Key Principals and the Members of a General Partner

The syndication model is structured in a way where it has no board of director, officers, or employees.

There are however key principals and other members of the company who will act in roles similar to those of directors, executive officers, and employees of a corporation.

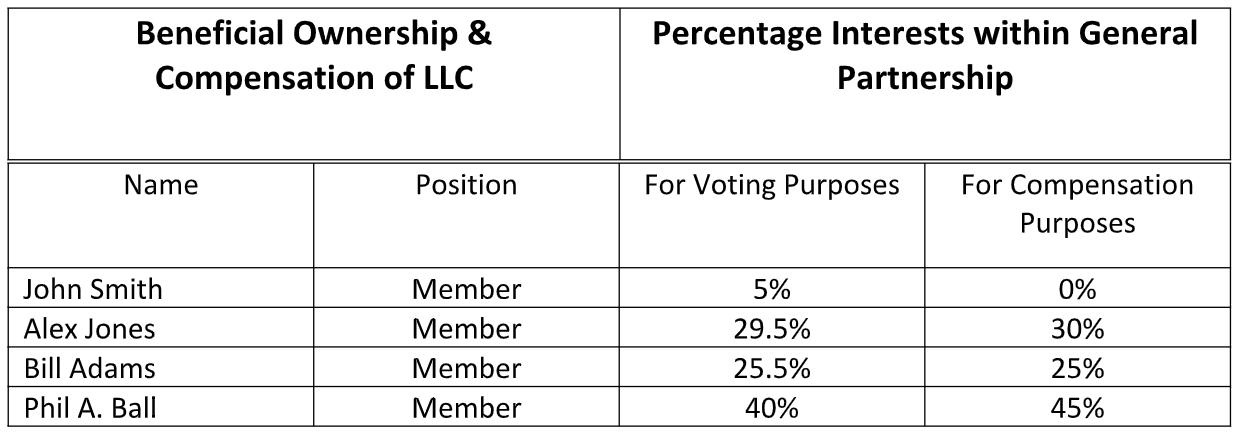

So how do key principals and the members get paid?

General partners and principals usually earn a compensation in the form of fees from the company, which are then distributed to its members based on the percentage of interest one has within the company (see table below).

However, it should be noted that every PPM attached to a syndication will look different. It’s imperative that you review, understand, and are comfortable with how the key principals and general partners are being paid out.

If you don’t understand, or have questions about the percentages of distribution, always ask the sponsor.

Investment Objective

Every smart real estate investor should enter into an investment with the end game (exit strategy) in mind, and syndicators aren’t any different.

Syndicators will often refer to the company’s investment strategy as the “investment objective”. This states how they plan to acquire, finance, manage, improve, and then sell the property.

So you need to understand how long the syndicator plans to hold the property and what the plan is for the exit strategy.

Typical hold patterns vary between three to ten years.

During the holding pattern your money is locked and you should be 100% comfortable with the allotted time.

Voting Rights

Limited partners are given limited voting rights and will not be able to vote on changes or handlings of the property’s operations.

However, the voting rights can be expressed if the limited partners would like to remove a general partner for good cause (as defined by the agreement), or to determine a new preferred exit strategy for the property.

This would typically require a majority vote and isn’t a common practice in syndications.

If you’ve vetted your sponsor carefully a coup will most likely not occur. It’s just something you should be aware of.

Depreciation Method to Be Used

In order for the company to maximize profits for investors it will typically use some form of depreciation, whether forced or not.

To optimize this process a cost segregation study is done to properties with a value over $1,000,000.

Depreciation should be passed on to limited partners, however not all sponsors do this. Depreciation deductions are one of the biggest advantages of investing in multifamily syndications. So investors should always ensure they’re getting their rightful share.

We highly recommend that all investors speak with their financial advisor to exercise and maximize these benefits.

* * *

Since PPMs are a bit dense, the average investor pays them very little attention.

Hopefully this article has armed you to become a more sophisticated investor, and to get the most out of your commercial real estate deals.

Key Takeaways:

- PPM shows how deal is structured,

- Who the partners are in the deal,

- The type of offering.

But for part 2 in the series, we will explore the most attractive aspect of the PPM…

How you, the investor, get paid.