PPM Risks & Rewards: How You Get Paid

Now that we’ve established the regulatory side, we can jump into the meat and potatoes.

Part 2 is all about that money.

We’ll discuss how both you and the syndicator get paid, as well as the associated risks:

- Sources and Uses of Proceeds

- Distributions to Limited Partners

- Fees and Compensation

- Conflicts of Interest

- Duties of the GP to LP

- Risk Factors

* Note: every PPM is unique, so you may not see EXACTLY the same thing as our examples, but we’re highlighting big-picture items that are going to be covered one way or another on basically every PPM you’ll read

Sources and Uses of Proceeds

It’s important to understand how the money works within a deal so you are never blindsided as an investor.

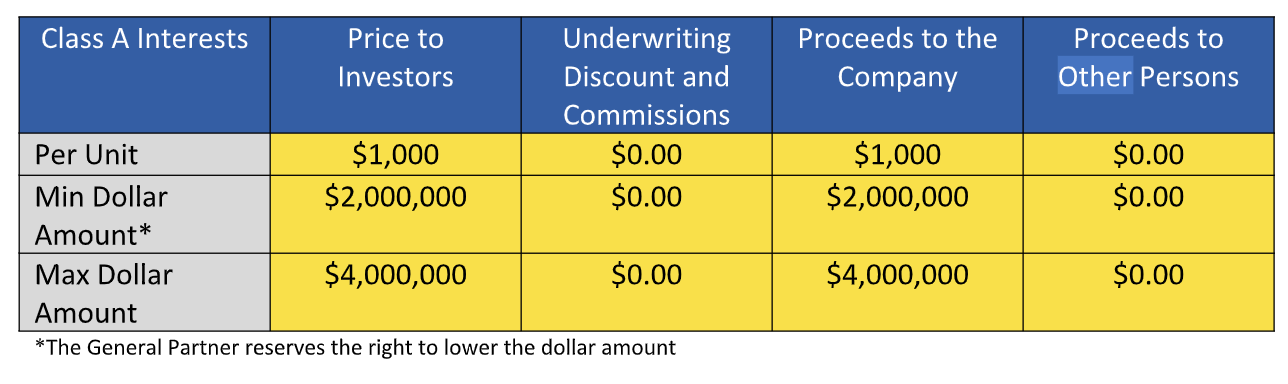

For every syndication model, there is a minimum and maximum dollar amount to be raised in order to acquire the property, with corresponding expenses.

Minimum Dollar Amount

This will tell you the low threshold of the capital raise, in order for the GP to use investor funds.

It also describes what happens when only this amount is raised (generally includes the GP deferring fees, advancing funds, or even seeking a loan from a third party).

Note that, usually, a GP can reduce this amount at their discretion.

Maximum Dollar Amount

This is the high end of the offering; the GP will not raise more money than this.

The offer can be terminated at any point before the maximum is raised.

Below is a typical table that would be used to show the minimum and maximum amounts.

Closing Costs

This section talks about how some of the proceeds of the offering will be used to pay the GP back for costs they may have incurred during the acquisition stage.

It will usually tell you where to look (in a table or appendix) to see the estimated closing costs of the deal. If the amount or usage is not clear to you (or seems too high or too low), you should ask the sponsor to elaborate.

Of course, like so many of the other metrics, the actual closing costs may differ from the original estimate.

In that case, you’ll also find a provision that states the GP will advance funds to close (if only the minimum dollar amount is raised), and, if so, how much interest they will charge until repaid.

This is unlikely to occur when sponsors conservatively underwrite a deal.

But it’s a possibility that you should be aware of, and should be included in the PPM.

Working Capital and Reserves

Sometimes there is excess cash raised above that needed to acquire the property.

Here you will find a description of what happens in that case. Typically the proceeds are held in a bank account to be used as working capital/reserves.

On the flip side, there are also provisions if only the minimum amount is raised.

So the PPM will include a description of how the property’s cash flow would be used instead, and how that may affect distributions.

Deferral Of Fees / Reimbursements

Much like closing costs above, there will be a plan in place if only the minimum amount is raised. This particular section talks about how the GP’s fees will be handled.

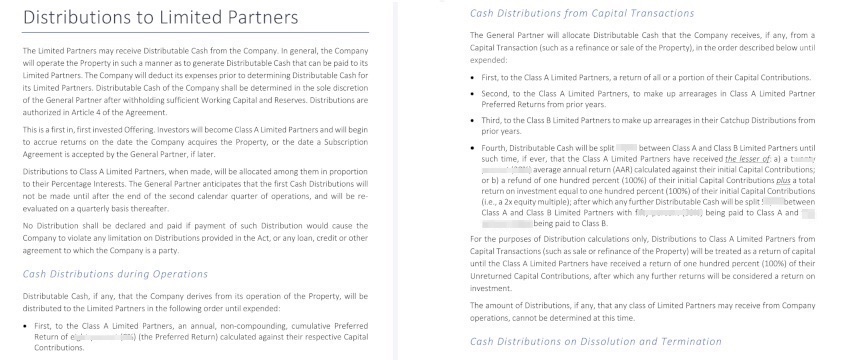

Distributions to Limited Partners

This is THE hot section of the PPM, from the point of view of you (the passive investor / Limited Partner).

Everyone always wants to know “when are the distributions”, “how much will they be”, etc.

Here you will learn how your returns will be paid out based on the cash flow of the operation, and in what proportion based on your investment.

It will also contain an estimate of when the first distribution will be paid out, and how often thereafter.

During Operations

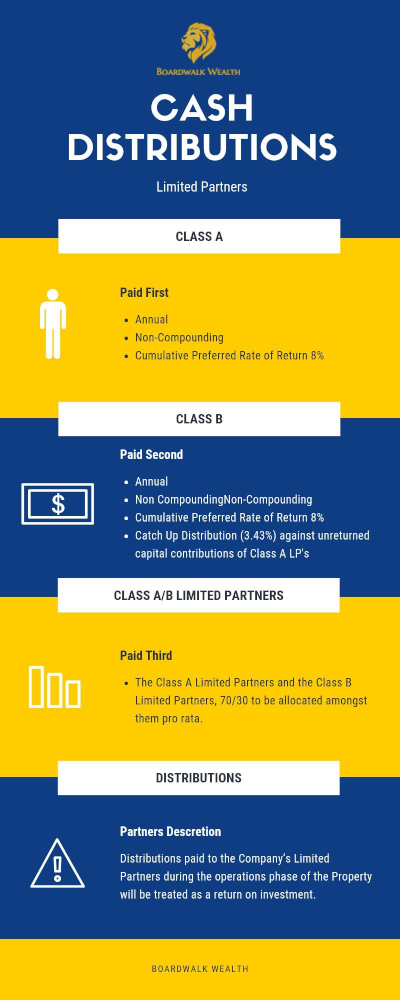

The distributable cash (from operations) will have an order in which it will go out, depending on the class of the Limited Partner.

Of course, no two deals are ever the same. So you should examine the payout structure outlined in each PPM.

Here is an example of a possible payout structure:

- First, to the Class A Limited Partners, an annual, non-compounding, cumulative Preferred Return of eight percent (8%) (the Preferred Return) calculated against their respective Capital Contributions.

- Second, to the Class B Limited Partners until they have received an annual, cumulative non-compounding cash distribution (the Class B Catch up Distribution) of 3.43% calculated against the Unreturned Capital Contributions of the Class A Limited Partners.

Note that this is equivalent to a 70/30 split between the Class A and Class B Limited Partners as shown below:

70 / 30 = 8 / 3.43 - Third, to the Class A Limited Partners and the Class B Limited Partners, 70/30 to be allocated amongst them pro rata.

Capital Transactions

But what happens if there is a refinance or the property is sold?

You’ll get a payout structure for this as well.

Just like the operational distributions, the LP (Class A) typically gets money first, and then the GP (Class B) gets some, and if there is anything left, the cash keeps getting split until the payouts reach a threshold.

Pay attention to all the numbers and return limits, and how they are affected by your original capital contribution.

Dissolution And Termination

This will tell you what happens to the company after the final settlement is made on the property.

Company assets will be distributed as outlined here.

It will usually refer to the next section about the GP’s fees as well.

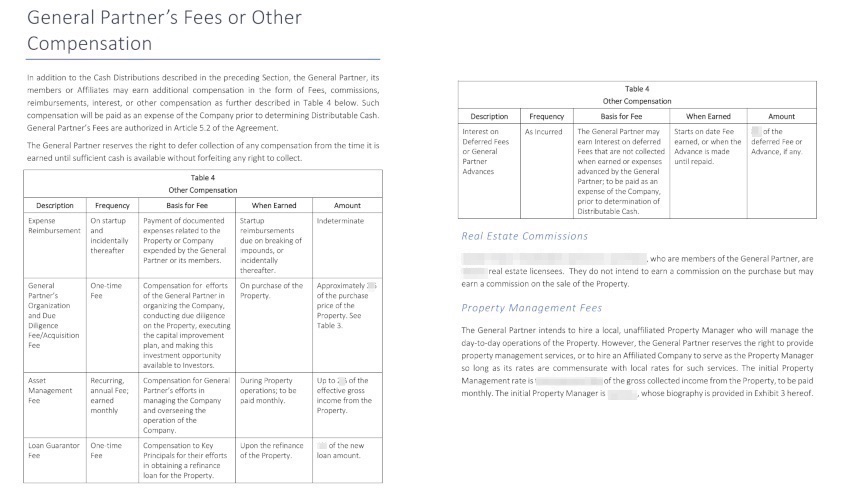

Fees and Compensation

The hardworking GP will want to collect some fees for bringing you such a lovely deal.

Usually they’ll outline how that works in a table like the one you see above.

That table also shows the most common types of fees you can expect to see in a PPM.

Property Management Fees

You’ll be able to read about the GP’s intentions to hire or provide property management services here.

Pay attention to the rate quoted, as well as an indication of who the property management company will be.

There may be an appendix or additional exhibit provided that goes into more detail about the Property Manager. You are generally trusting the GP to choose a competent and efficient PM, but it never hurts to read a little about them and make sure nothing sounds out of order.

Note that there are usually two types of property management arrangements:

- The GP hires a local or regional company.

- The GP is vertically integrated and has a property management division that will handle operations.

Conflicts of Interest

This is just to make you aware of realistic potential situations that may come up, that could be seen legally as conflicts of interest.

It sounds worse than it is, because (for example) the top operators in a submarket will often hold a few “competing” properties in the area to leverage economies of scale on property management. This is usually seen as a benefit in a deal, even if it could be coldly defined as a “conflict of interest”.

A few sections of note here are:

General Partner May Be Involved in Similar Investments

This one is warning you that the GP may be involved in other deals. It’s an amusing point because most investors prefer a syndicator with experience, who has a portfolio they can inspect.

The main point of contention is that the GP may have spread themselves too thin, and is paying attention to another property at the cost of attention to your investment. This speaks more to the trustworthiness and organization of the GP, of course.

General Partner May Raise Capital for Others

Just like the previous point, if your GP is active within a larger network of commercial investors, it’s fairly common that they have helped a colleague raise money on a deal (and will do so in the future).

From the point of view of a diligent syndicator, it may be their chance to offer their investors access to a vetted member of their business circle who was able to score a good deal in between their own offers.

Duties of the GP to LP

Fiduciary Duties of the General Partner to the Company

These are the ways that the GP is legally obligated to act in your interest.

A lot of it is standard boilerplate, but here are some general things you should be able to expect the GP to do:

- use their best efforts when acting on the Company’s behalf

- not act in any manner adverse or contrary to the Company’s interests

- exercise all of the skill, care, and due diligence at their disposal

Indemnification of General Partner

This is fancy legalese that boils down to one simple point:

The General Partner will only be held responsible if they engage in willful misconduct, bad faith or fraud.

This does not excuse the General Partner from liabilities arising from violations of the Securities Act, as the SEC is the arbiter in that case.

In other words, the General Partners cannot be held liable for damages that arise from the regular course of business events or unforeseen events.

Risk Factors

You are probably already aware of the many risks associated with any type of investing.

What follows is common sense, but it will help you get a scope on how they apply to multifamily deals in particular.

We’ve chosen a few of the most commonly included risk factors.

The General Partner’s Overall Abilities

The success of the company depends on the general partner’s ability to manage the asset from beginning to end:

- Acquisition of property

- Manage

- Operate

- Finance

- Disposition

Lack of Control and Limited Voting Rights

As a Class A Limited Partner, you don’t have control over the Company’s day-to-day operations.

And your voting power will be limited to very specific cases (eg. to replace the General Partner for Good Cause), that will rarely happen.

Limited Transferability and Liquidity

Limited Partners need to understand the holding period for the asset, as well as its liquidity.

It’s important to note that there’s no secondary market to dispose of shares. This is an investment that requires several years from beginning to end. It is illiquid.

Lack of Capital

Unexpected expenses could arise causing a lack of capital which could hinder the business plan and delay the overall objectives.

Risk of Not Receiving Any Distributable Cash

Market conditions could shift along with unexpected capital expenditures thus affecting the business plan. There can only be distributions if there is enough cash flow to pay them.

Lack of Diversification

The company has no assets other than the property and no plans to diversify its assets. Therefore, the success of the company will be based on its operations and management.

Investors Not Represented by Independent Counsel

Limited Partners are not represented and have not been represented by independent lawyers, and should seek their own counsel.

Due Diligence May Not Uncover All Material Facts

This is saying that there are no guarantees that the seller has not misled the General Partner, or is even possibly just ignorant altogether.

A good GP digs in and does their homework. Although there are often very reasonable discoveries made after a few months of operation, they should not sour a deal (but they could… hence the risk factor).

Financial Projections May Be Wrong

The investment summary contains metrics like projected annual ROI returns. Since these are just projections, you have to be prepared that they may not actually be realized.

It’s rare that the numbers are drastically off.

But it’s helpful to think of syndicators in two camps: those who are optimistic about returns, and those who are very conservative about returns. We fall in the latter camp.

So this may even mean, in practice, that your returns will be higher than you planned for.

Either way, the exact numbers are not guaranteed.

Risks Related to Section 8 Tenants

Section 8 tenants are subsidized by the government. If the company decides to rent to them, it’s going to have to deal with more scrutiny under the local housing authority.

This includes passing an annual housing inspection on the property, and for each tenant to re-qualify yearly.

Any failures involved in inspection or qualification could dramatically affect cash flow, operations, and ultimately your distributions.

Risks Related to Leveraging the Property

There is always the risk that monthly income will not meet monthly debt service, or that sales proceeds will not be enough to pay off the balance of financing.

Class A LPs could suffer anything from total loss of capital to just receiving a lot lower returns than they expected.

There is nothing in this section that protects you from an over-zealous syndicator with too-optimistic underwriting, so all the text here is just common sense. The real work is done when you vet your deal sponsor.

Risks Related to Owning Real Estate

Generally, there are several risks associated with real estate investing:

- Changing environmental regulations

- Changes in the demand for or supply of a competing property

- Local economic factors

- Uninsured losses

- Inability to get permits

- Environmental hazards

- Failure of the lender to approve the loan

- Loss of liquidity in markets

- Inability to collect rents

- Acts of God or other calamities

The point here is to understand all the risks associated with this investment class. These are just some examples (along with many others) that possibly could affect your investment.

Is real estate a less volatile asset? Yes. Is there still a risk in multifamily apartment investing? Yes.

It’s always important that YOU as the investor do your own due diligence and familiarize yourself as much as possible.

* * *

Cash is king in real estate!

Now you as the investor have a clearer understanding of how you get paid, fees associated with the deal, and the risk factors.

You’ve acquired a lot of information, but there’s one last thing to truly understand the PPM.

Part 3 will cover your role as a limited partner in a syndication deal.

Sadly it’s not just to “sit back and collect cash”.

But nearly. So read on to learn just how passive a passive investor can be, and what is actually expected of you once you invest.